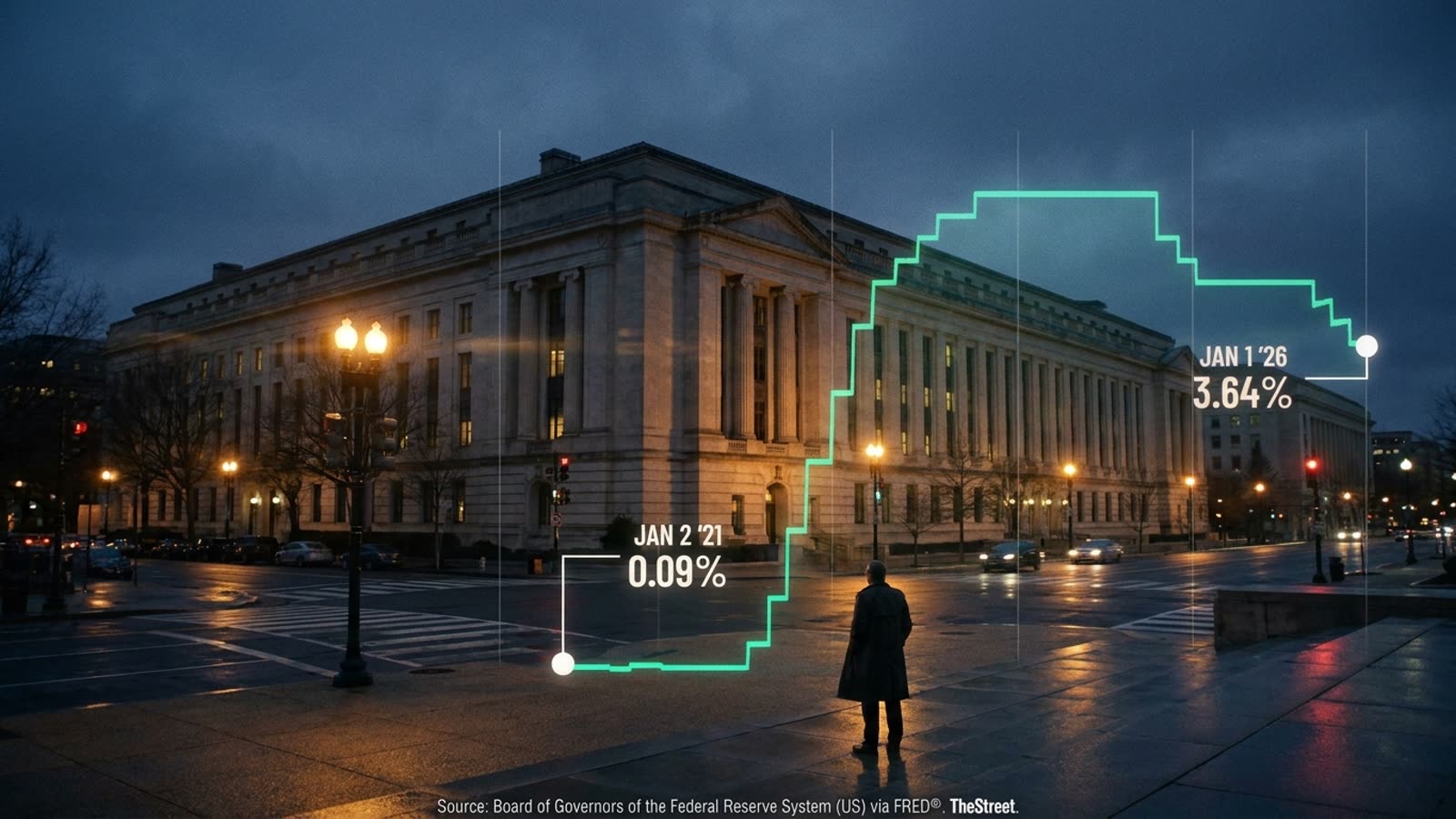

The Federal Reserve has spent the first half of 2026 in a holding pattern that would make air traffic controllers nervous. Inflation proved stickier than expected through Q1, labor markets refused to crack, and Chair Powell's "data dependent" mantra began to sound less like prudent caution and more like institutional paralysis. This week's triple release of PCE inflation, weekly jobless claims, and housing data will either vindicate the patience or expose it as a policy error.

The stakes are higher than the usual monthly data theater. Markets have priced in roughly 50 basis points of cuts by year-end, down from the 100-plus basis points traders expected in January. Each incoming print now carries disproportionate weight, capable of swinging rate expectations by a full quarter-point cut in either direction.

The PCE puzzle

Core PCE — the Fed's preferred inflation gauge — has been maddeningly consistent, hovering in the 2.6-2.8% range for months. The central bank needs to see a convincing move toward 2% before it can justify easing, but the economy keeps generating just enough price pressure to keep that target tantalizingly out of reach. A print above 2.7% would likely push rate cut expectations into 2027 territory. Anything below 2.5% would trigger a rally in rate-sensitive assets and reignite the summer cut narrative.

Labor's quiet deterioration

Weekly jobless claims have been the canary that refuses to die. Initial claims have crept higher over the past two months — not dramatically, but persistently enough to suggest the labor market's famous resilience may finally be fraying. Continuing claims tell a more concerning story: workers who lose jobs are taking longer to find new ones. If this week's numbers confirm the trend, the Fed faces the uncomfortable possibility that it has already waited too long.

Housing's double message

The housing data presents its own contradiction. Prices remain elevated in most metros, supporting the wealth effect that keeps consumers spending. But transaction volumes have collapsed, mortgage applications are at multi-decade lows, and builders are offering concessions that don't show up in headline price indices. The sector is frozen rather than crashing — a distinction that gives the Fed cover to wait but doesn't resolve the underlying affordability crisis.

Our take

The Fed's 2026 strategy amounts to hoping the data eventually cooperates. That's not monetary policy; it's wishful thinking with a press conference. Powell's committee has become so traumatized by the 2021-2022 inflation miss that it now risks the opposite error: keeping policy restrictive long enough to break something that can't be easily fixed. This week's numbers won't resolve the debate, but they'll reveal whether the landing is still soft or just hasn't hit the ground yet.