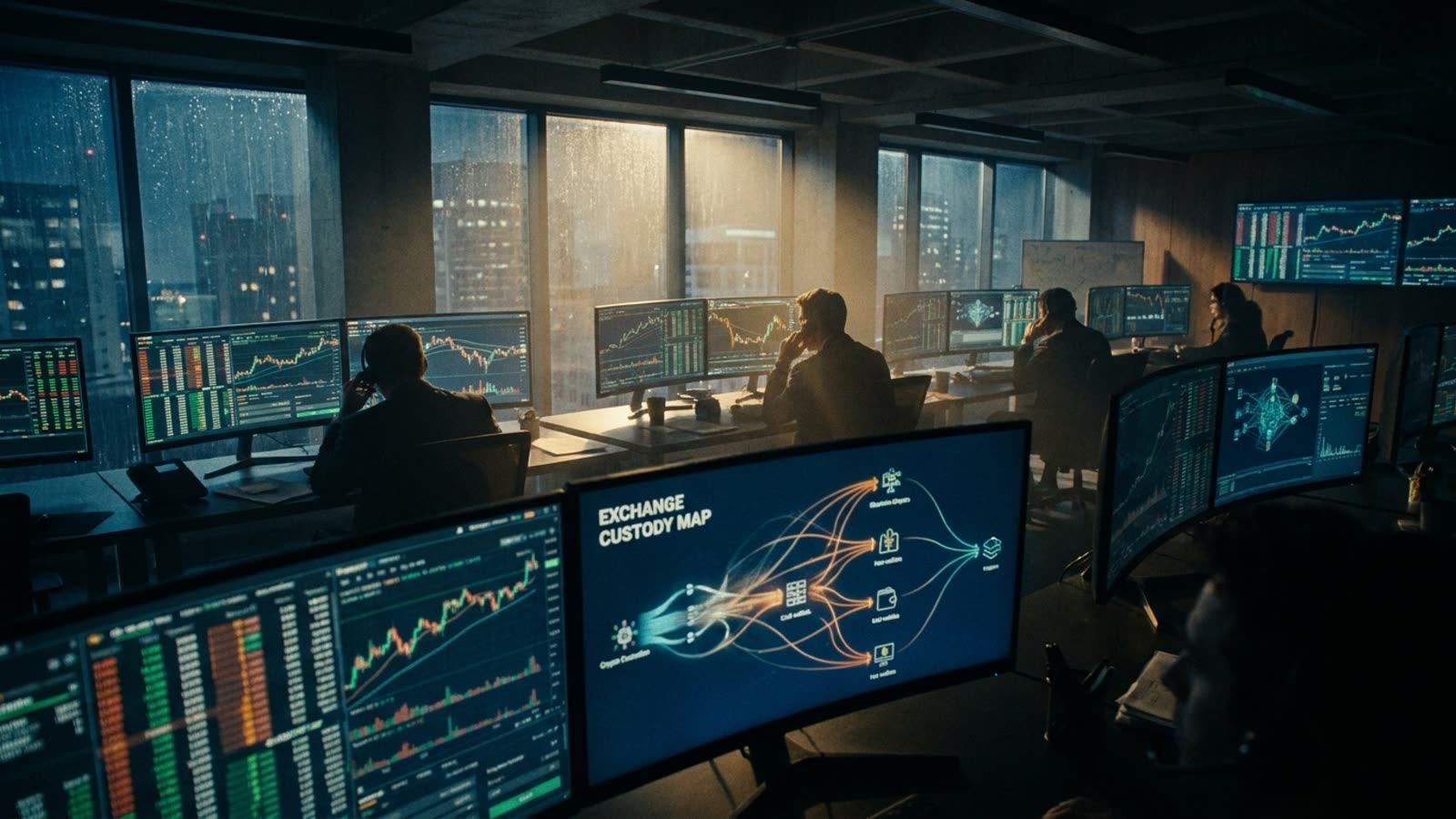

When you purchase cryptocurrency on a major exchange, you receive a number on a screen. That number represents your balance in the exchange's internal database. It does not represent coins sitting in a wallet with your name on it, waiting patiently for your next move. The distinction sounds pedantic until an exchange freezes withdrawals, files for bankruptcy, or simply vanishes—at which point the difference between owning cryptocurrency and owning a claim on an exchange's solvency becomes painfully clear.

The architecture of centralized exchange custody is both more sophisticated and more precarious than most users appreciate. Understanding it requires abandoning the intuitive model of a bank vault and embracing something closer to a massive, constantly rebalancing ledger of IOUs backed by a smaller pool of actual assets.

The hot-cold divide

Exchanges maintain two fundamental categories of wallets: hot and cold. Hot wallets are connected to the internet and handle the constant flow of deposits and withdrawals. They contain whatever liquidity the exchange needs for immediate operations—typically a small percentage of total holdings. Cold wallets are air-gapped, often distributed across multiple physical locations, sometimes involving elaborate security theater with Faraday cages and biometric access.

The ratio between hot and cold storage varies by exchange and market conditions. During periods of heavy withdrawal demand, exchanges must move funds from cold to hot, a process that can take hours and requires multiple signatories. This is why withdrawal delays often precede exchange collapses: the hot wallet empties, cold transfers become bottlenecked, and the gap between user balances and actual reserves becomes impossible to bridge.

The omnibus problem

Most exchanges do not maintain individual wallets for each user. Instead, they pool customer funds into omnibus wallets—large aggregated addresses that hold assets on behalf of thousands or millions of accounts. Your "balance" is an entry in the exchange's proprietary database, not a segregated allocation on the blockchain.

This creates efficiency but introduces counterparty risk. When an exchange commingles customer funds with operational capital, or lends out deposits to generate yield, or simply mismanages liquidity, the omnibus structure means every user's claim is only as good as the exchange's overall solvency. The blockchain itself has no knowledge of your specific entitlement.

Proof of reserves and its limits

After high-profile collapses, the industry embraced "proof of reserves"—cryptographic attestations that an exchange controls certain wallet addresses. The concept sounds reassuring until you examine what it actually proves: that an exchange held specific assets at a specific moment. It does not prove the absence of liabilities, the legitimacy of user balance data, or the persistence of those reserves five minutes after the attestation.

More sophisticated approaches involve Merkle trees that allow users to verify their balance is included in the total, but these remain voluntary, inconsistently implemented, and easily gamed by exchanges that borrow assets temporarily to pass audits.

Our take

The crypto industry built itself on the promise of trustless systems, then recreated the exact trust dependencies it claimed to eliminate. Centralized exchanges are banks without deposit insurance, brokerages without regulatory oversight, and custodians without fiduciary obligations—all wrapped in the aesthetic of decentralization. Users who understand this architecture can make informed choices about the tradeoffs between convenience and custody risk. Users who don't are simply hoping their exchange is one of the honest ones.