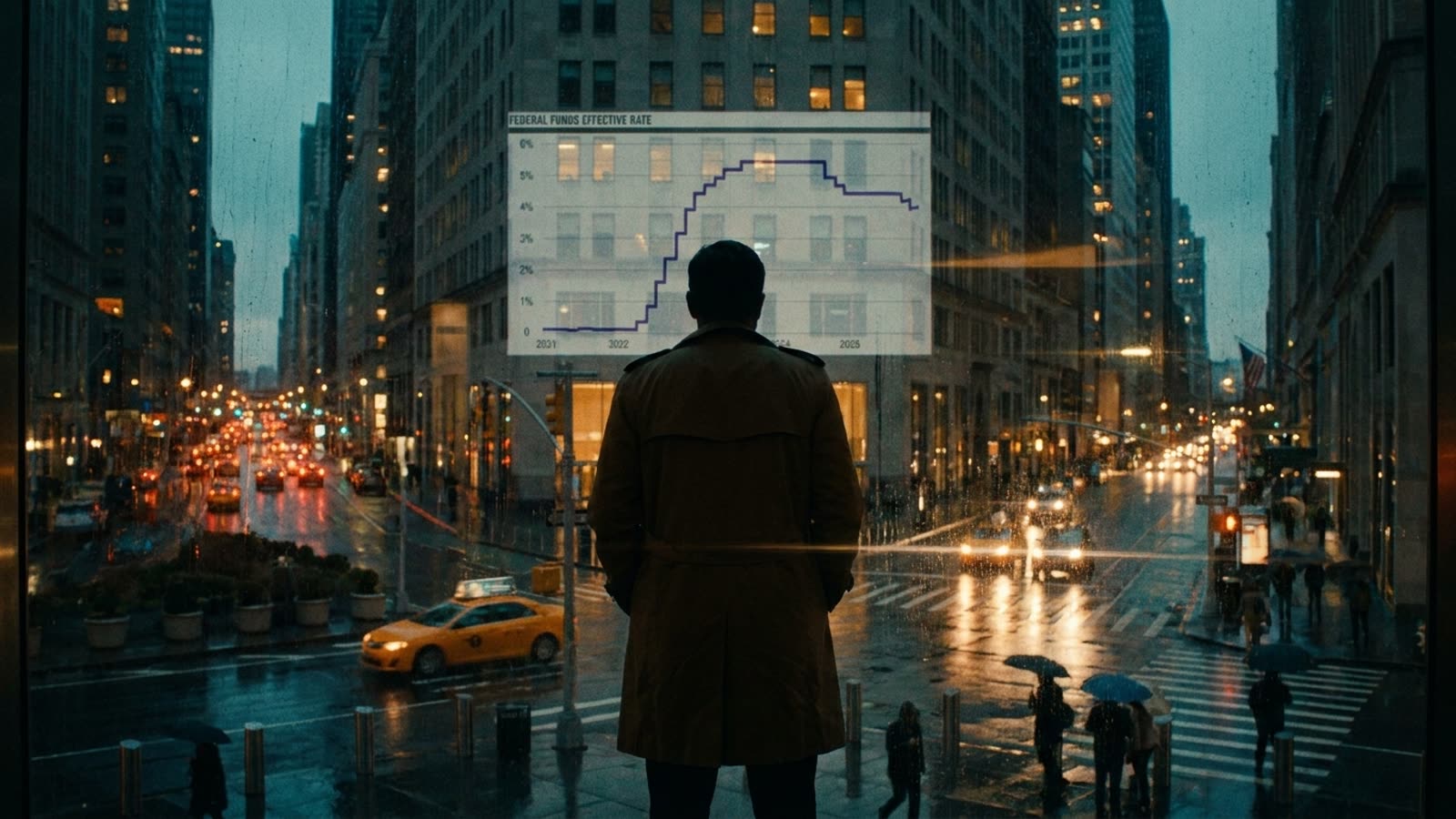

Wall Street has spent the spring building an elaborate castle of rate-cut expectations on foundations the Federal Reserve has repeatedly warned are made of sand. This week, the PCE inflation report—the Fed's preferred price gauge—will either validate the market's optimism or expose it as wishful thinking.

The disconnect between trader positioning and Fed rhetoric has rarely been this stark. Futures markets are pricing in at least two quarter-point cuts by year's end, with the first potentially arriving as early as July. Meanwhile, Fed officials have maintained their higher-for-longer stance with the consistency of a metronome, citing sticky services inflation and a labor market that refuses to crack.

The data gauntlet

Thursday's PCE release carries outsize significance precisely because the Fed has made clear it needs sustained evidence of disinflation before moving. Core PCE—stripping out volatile food and energy—has hovered stubbornly above the 2% target for months. A reading that confirms this persistence would force traders to reprice their summer cut dreams; a surprise decline would vindicate the bulls and likely send risk assets higher.

The week also brings initial jobless claims, which have remained remarkably low despite high-profile layoff announcements in tech and media. The housing data adds another dimension: mortgage rates above 6.5% have frozen much of the market, yet prices remain elevated in most metros, creating a peculiar stalemate that neither supports nor undermines the inflation narrative cleanly.

The Middle East variable

Complicating the picture is the emerging détente between Washington and Tehran. Oil's recent plunge on peace hopes has eased energy-related inflation pressures, potentially giving the Fed cover to cut even if other components remain elevated. But central bankers are notoriously reluctant to react to geopolitical developments that could reverse overnight. A deal that falls apart would send crude—and inflation expectations—surging again.

Our take

Markets are playing a dangerous game of chicken with a central bank that has shown no inclination to blink. The Fed burned its credibility calling inflation "transitory" in 2021 and has since overcompensated with hawkish resolve. Chair Powell would rather be late to cut than early and wrong again. This week's data probably won't be bad enough to kill rate-cut hopes entirely, but it's unlikely to be good enough to justify the aggressive easing priced into futures. The smart money is on disappointment—not disaster, just the slow, grinding realization that summer cuts were always more fantasy than forecast.