The autonomous vehicle industry has spent a decade promising that self-driving cars would be safer, cheaper, and more ubiquitous than human-operated transport by now. In 2026, the reality check has arrived—not from the technology itself, but from the regulators who once gave it remarkably free rein.

Across the United States, a pattern is emerging: jurisdictions that welcomed robotaxi pilots with minimal restrictions are now imposing new requirements, pulling permits, or simply declining to expand operating zones. The shift represents less a crisis of faith in autonomy than a belated acknowledgment that the regulatory framework never matched the ambition of the companies deploying these vehicles.

The permissive era ends

For most of the past decade, state and federal regulators approached autonomous vehicles with deliberate restraint. The logic was straightforward: impose too many rules too early, and you risk strangling innovation before it matures. California, Arizona, and Texas competed to attract AV companies with light-touch oversight, viewing themselves as laboratories for a transformative technology.

That approach produced valuable data—and a growing catalog of incidents that exposed its limitations. Vehicles blocking emergency responders, struggling with construction zones, and occasionally colliding with stationary objects generated headlines and, more importantly, generated questions about whether self-certification and voluntary safety commitments were sufficient.

The National Highway Traffic Safety Administration, which long resisted prescriptive rules for AVs, has begun signaling a more interventionist posture. State DMVs are requiring more granular incident reporting. Insurance regulators are asking harder questions about liability frameworks that remain genuinely unsettled.

The technology gap persists

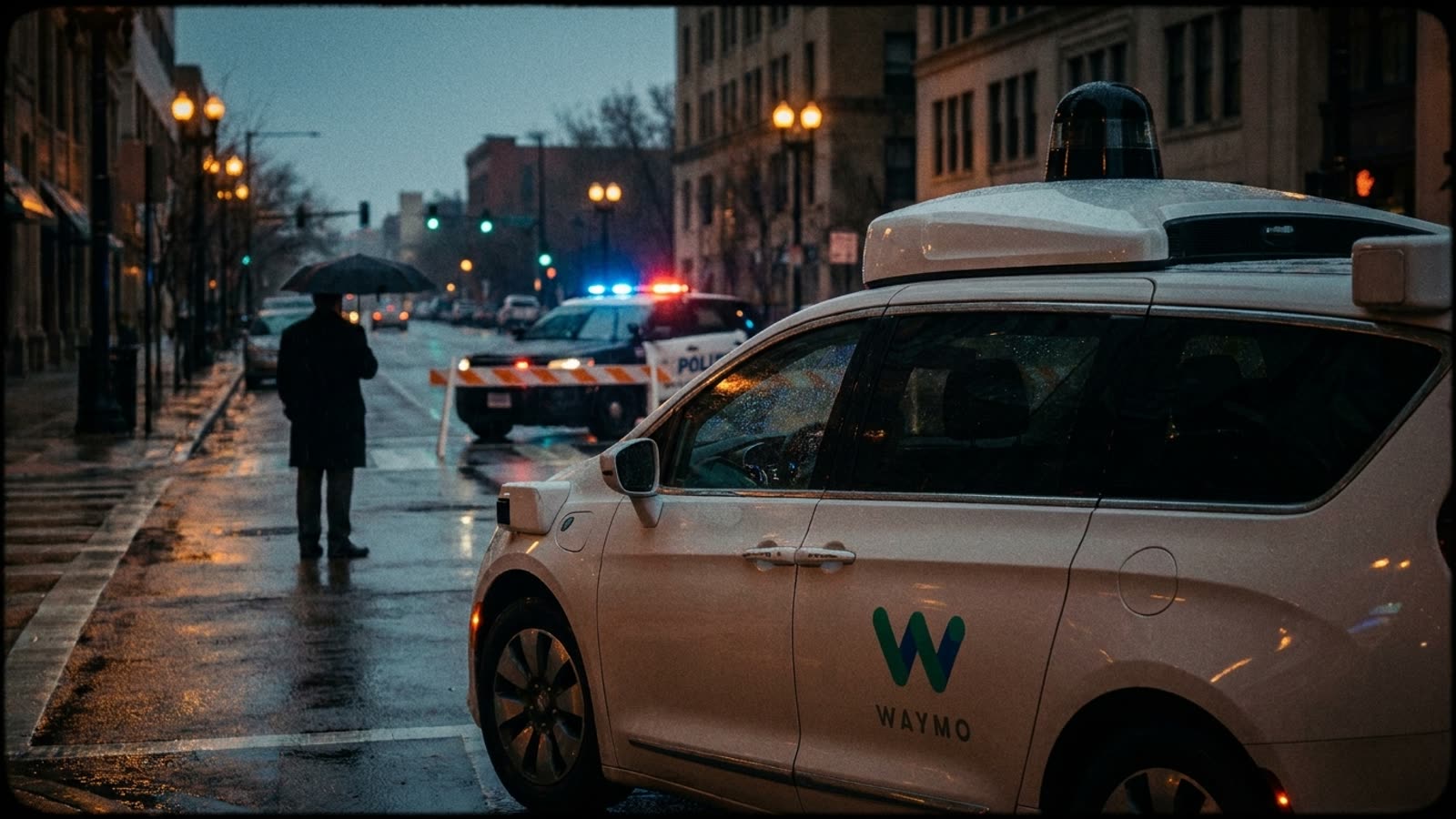

The regulatory tightening reflects a dawning recognition that the technological challenges of full autonomy remain formidable. The industry's own timelines have slipped repeatedly. Waymo operates commercially in a handful of geofenced urban zones. Cruise suspended operations entirely after a 2023 incident and regulatory backlash. Tesla's Full Self-Driving remains, despite the name, a driver-assistance system requiring constant supervision.

None of this means autonomy is a dead end. The technology genuinely works in constrained environments with good weather, mapped roads, and predictable traffic patterns. But the leap from "works in Phoenix suburbs" to "works everywhere humans drive" has proven far larger than early boosters anticipated.

Investors have noticed. Valuations for pure-play AV companies have compressed dramatically from their peaks. The survivors are increasingly those with patient capital and realistic deployment horizons measured in decades rather than quarters.

Our take

The robotaxi reality check is healthy, not fatal. Autonomous vehicles will eventually transform transportation—the underlying technology continues to improve, and the economic logic of removing the driver remains compelling. But the industry's credibility suffered from years of overpromising, and regulators who enabled that hype cycle are now course-correcting. The companies that thrive will be those that welcome scrutiny rather than resent it, understanding that public trust is the scarcest resource in this particular race.