The phrase "proof-of-stake" has become so ubiquitous in cryptocurrency discourse that it functions more as tribal signifier than technical description. Enthusiasts invoke it to distinguish their preferred networks from Bitcoin's energy-intensive mining; critics dismiss it as plutocracy with extra steps. Both camps tend to skip past what the mechanism actually does, which is a shame, because the underlying logic is elegant and surprisingly old.

At its core, proof-of-stake solves the same problem that proof-of-work solves: how do you get a network of strangers, with no central authority, to agree on which transactions are valid and in what order they occurred? In proof-of-work, the answer is computational effort — miners burn electricity to prove they did expensive work, and the network trusts the chain with the most accumulated work. In proof-of-stake, the answer is economic exposure — validators lock up capital as a bond, and the network trusts them because they have something to lose.

The ancient logic of the bond

This is not a novel idea. Medieval merchants posted bonds before entering foreign markets. Contractors put up performance guarantees. The principle is identical: if you have skin in the game, your incentives align with honest behavior. Proof-of-stake formalizes this intuition in code. Validators deposit cryptocurrency into a smart contract, propose and attest to blocks, and face automatic penalties — called "slashing" — if they behave dishonestly or negligently. The collateral is not symbolic; it can be partially or fully destroyed by the protocol itself.

The elegance lies in the self-enforcement. No court, no regulator, no reputation system is required. The validator's own capital serves as both license and liability. Misbehave, and the protocol confiscates your stake algorithmically. This creates a direct, measurable cost for attacks that would otherwise be cheap to attempt.

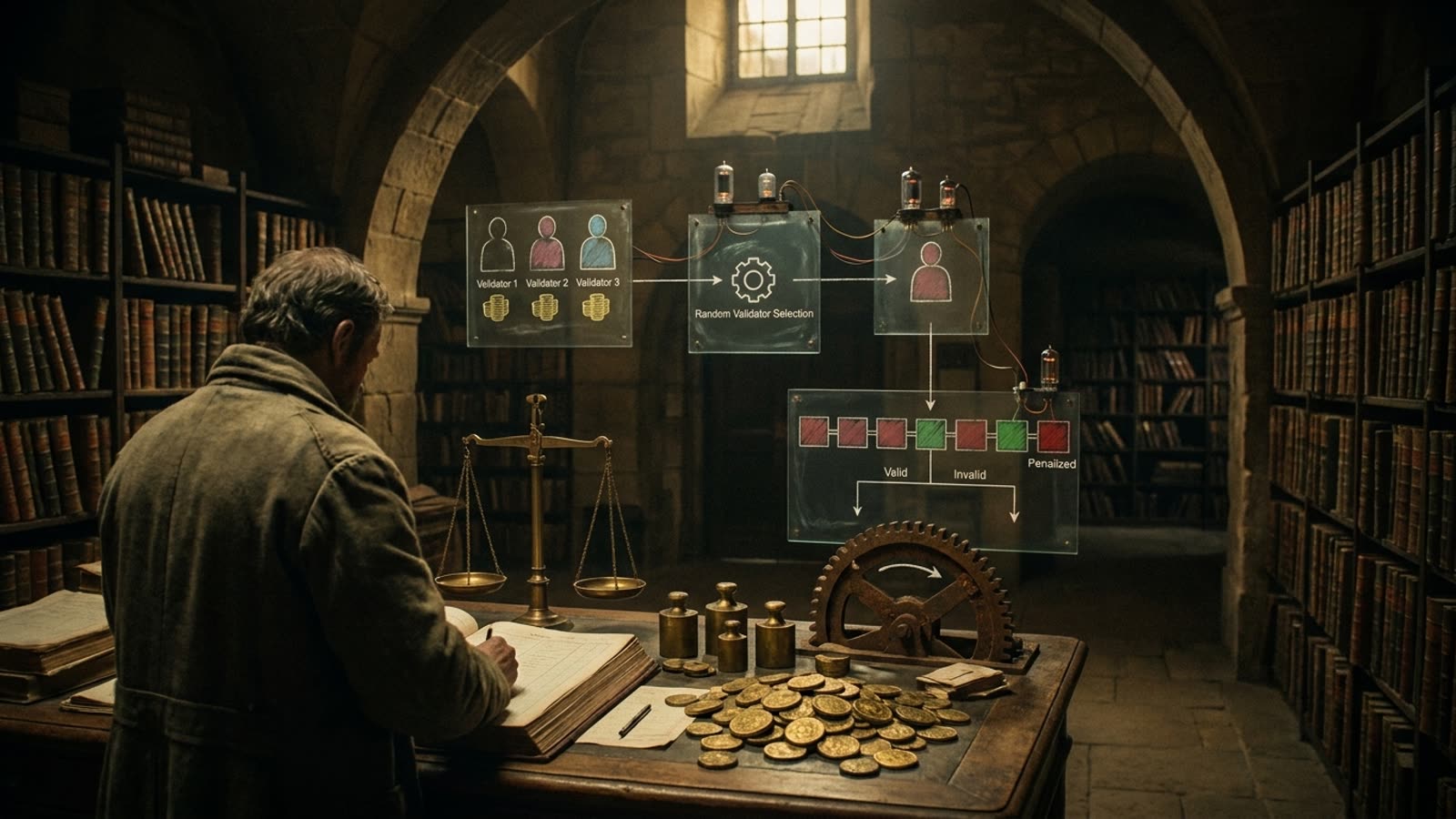

What validators actually do

A common misconception is that staking means passively earning yield for doing nothing. In reality, validators run infrastructure. They maintain nodes that stay synchronized with the network, propose new blocks when selected by the protocol's randomness function, and attest to the validity of blocks proposed by others. The randomness is weighted by stake — larger deposits mean more frequent selection — but it is not deterministic. A validator with one percent of total stake will, on average, propose one percent of blocks, but the timing is unpredictable enough to prevent manipulation.

The attestation process is where consensus actually forms. When enough validators attest to a block, it becomes "finalized" — irreversible under normal conditions. This finality is probabilistic in some designs and absolute in others, but the key point is that it emerges from economic commitment, not computational competition. Validators who attest to conflicting blocks lose their deposits. The protocol does not care why they did it; the punishment is automatic.

The tradeoffs nobody advertises

Proof-of-stake is not without costs. The most obvious is that it concentrates influence among those who already hold capital. Wealthy participants can stake more, earn more rewards, and compound their advantage over time. Defenders argue that proof-of-work has the same dynamic with mining hardware, and they are not wrong, but the critique stands. Stake-weighted systems are, by design, capital-weighted systems.

There is also the question of long-range attacks. In proof-of-work, rewriting history requires re-doing all the computational work since the target block — an expense that grows with time. In proof-of-stake, an attacker who acquires old private keys could theoretically create an alternate history without ongoing cost. Most modern implementations address this through "checkpointing" — periodic snapshots that the network treats as canonical — but the solution introduces its own trust assumptions.

Our take

Proof-of-stake is neither revolution nor scam. It is a different set of tradeoffs, one that favors energy efficiency and faster finality at the cost of increased capital concentration and more complex security assumptions. Understanding it requires no mysticism, only a willingness to think about incentives clearly. The mechanism works because validators are not trusted — they are bonded. That distinction matters more than most of the discourse around it suggests.