The S&P 500 is flirting with all-time highs, tech giants are adding hundreds of billions in market capitalization, and financial media is awash in triumphalist language about wealth creation. Yet consumer sentiment surveys tell a different story: Americans remain deeply pessimistic about their economic prospects, and the disconnect is not a puzzle—it is a feature of how modern prosperity is distributed.

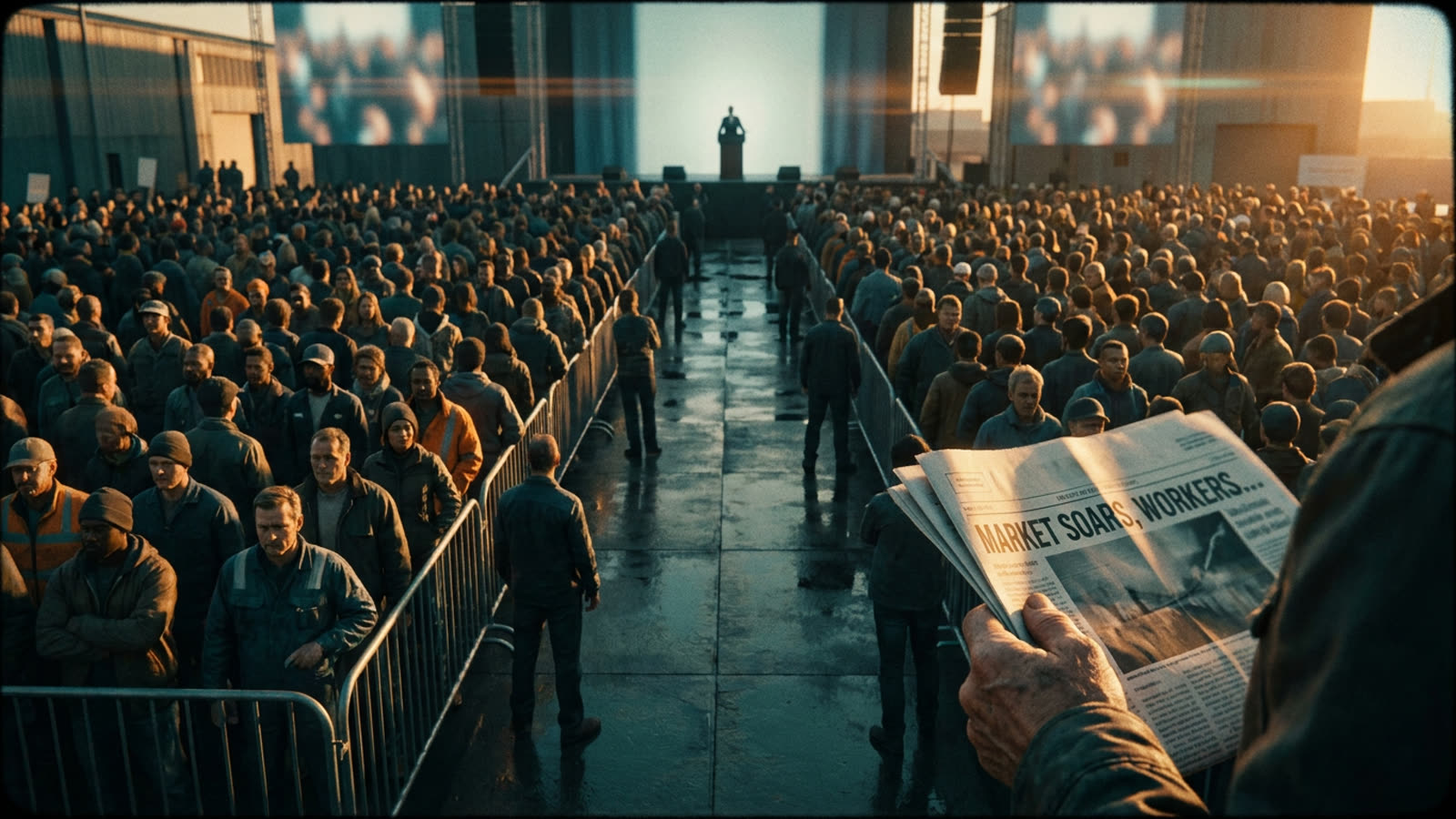

The arithmetic is stark. The wealthiest ten percent of American households own roughly 93 percent of all equities, a concentration that has only intensified over the past two decades. When the Nasdaq climbs, their net worth climbs with it. For the median household—whose wealth is overwhelmingly tied to home equity and whose retirement savings, if any, sit in modest 401(k) balances—the rally registers as background noise at best and, at worst, as a reminder of an exclusive party they were never invited to.

The wealth effect in reverse

Economists have long studied the "wealth effect," the tendency of rising asset prices to boost consumer spending as people feel richer. Less discussed is its inverse: the psychological toll on those excluded from the gains. When housing costs, healthcare, and education continue to outpace wage growth, watching others get rich on paper can feel like falling behind even when your paycheck stays the same. The result is a bifurcated economy where GDP growth and stock indexes tell one story while kitchen-table finances tell another.

The rally's beneficiaries are not evenly distributed by geography or demography. Coastal knowledge workers with equity compensation and diversified portfolios have seen their wealth compound. Meanwhile, service-sector employees in the interior—many of whom never recovered the ground lost during the pandemic—are contending with sticky inflation on essentials and interest rates that make borrowing more expensive than at any point in their adult lives.

Why the rally feels hollow

Part of the dissonance stems from what is driving the market. The current surge is heavily weighted toward a handful of mega-cap technology names, many of them riding enthusiasm for artificial intelligence. This is not the broad-based bull market of the late 1990s, when day traders and retail investors felt like participants. Today's gains are concentrated in stocks that most retail portfolios underweight, and the passive index funds that do capture them are held disproportionately by the already-wealthy.

There is also a timing mismatch. The Federal Reserve's aggressive rate-hiking cycle punished borrowers—homebuyers, credit-card holders, small-business owners—while eventually rewarding equity holders as markets priced in a soft landing. Those who needed cheap capital to build wealth were squeezed; those who already had capital watched it grow.

Our take

The stock market is not the economy, but it is increasingly the economy for a specific class of Americans. Policymakers and pundits who cite equity indexes as evidence of national prosperity are speaking a language that most households do not recognize. Until wage growth, housing affordability, and retirement-account participation catch up to asset-price inflation, the rally will continue to feel like someone else's good news—and the misery index will remain stubbornly high even as the Dow sets records.