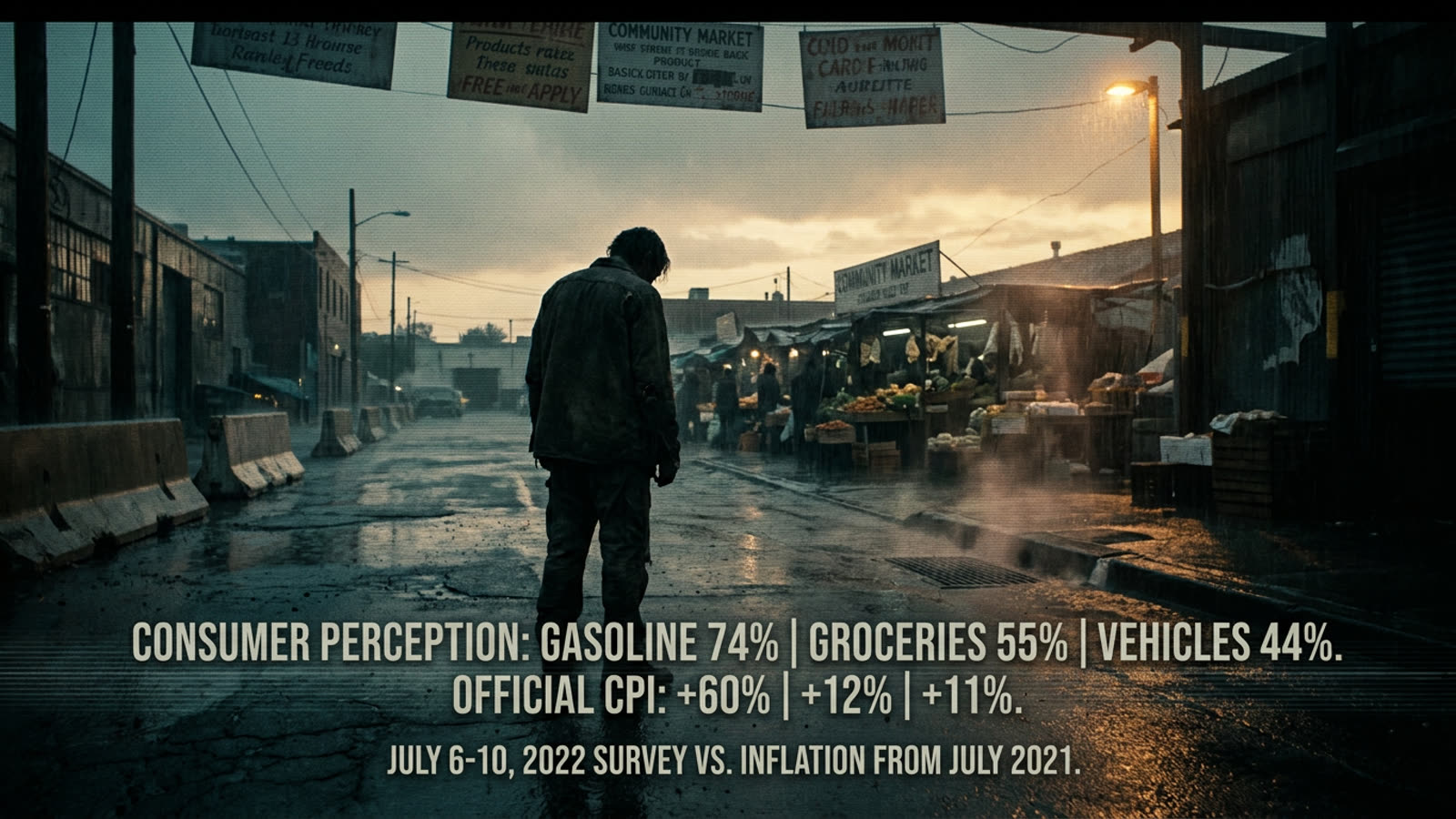

Few phrases in economics carry as much aspirational weight as the soft landing. The term conjures images of a pilot easing a jumbo jet onto the tarmac—passengers undisturbed, coffee cups still upright. In monetary policy, it describes a central bank raising interest rates just enough to tame inflation without tipping the economy into recession. It sounds reasonable. It is also, by most historical accounts, extraordinarily rare.

The appeal is obvious. Recessions destroy jobs, shutter businesses, and leave scars on household balance sheets that can take a generation to heal. If policymakers could simply dial down demand with surgical precision, the trade-off between price stability and full employment would dissolve. The Federal Reserve, the European Central Bank, and their peers around the world have all, at various points, claimed to be engineering exactly this outcome. The record, however, is less flattering than the rhetoric.

The arithmetic of a narrow runway

A soft landing requires threading a needle that keeps moving. Central banks must guess how much economic activity is too much, how quickly rate hikes will bite, and how long households and firms will tolerate higher borrowing costs before pulling back. Each variable is uncertain; together, they compound into a forecasting problem that humbles even the most sophisticated models. Monetary policy operates with famously long and variable lags—a phrase coined by Milton Friedman that remains uncomfortably accurate. By the time data confirm that rates are too high, the damage may already be baked in.

The celebrated soft landing of the mid-1990s in the United States is often cited as proof of concept. The Fed doubled rates over roughly a year, inflation cooled, and unemployment barely budged. Yet many economists attribute that success less to Alan Greenspan's deft touch than to a productivity boom driven by information technology—an exogenous tailwind that central bankers neither predicted nor controlled. Strip away the luck, and the skill becomes harder to isolate.

Why markets want to believe

Financial markets have a structural incentive to price in soft landings. Equity valuations depend on future earnings, which depend on consumers and businesses continuing to spend. A recession reprices risk assets violently downward; a soft landing lets the party continue with only a modest hangover. Analysts and strategists therefore tend to assign soft-landing scenarios higher probabilities than history would justify, in part because their clients prefer optimism and in part because pessimism is career risk.

This bias creates a feedback loop. When markets rally on soft-landing hopes, wealth effects support consumption, which in turn makes the soft landing more plausible—until it doesn't. The pattern has repeated across cycles: confidence builds, positioning becomes crowded, and the eventual disappointment, when it arrives, is sharper for having been so widely dismissed.

Our take

The soft landing is less a policy tool than a narrative device—a story central bankers tell to justify tightening and markets tell to justify valuations. Occasionally the story comes true, usually because forces outside the control room intervene. That does not make the pursuit foolish; it makes it humble. The honest answer to whether a soft landing is achievable is almost always the same: perhaps, but probably not in the way anyone expects.