Insurance underwriting has always been an exercise in informed pessimism. For centuries, the job has required humans to stare at applications, medical records, property assessments, and actuarial tables, then render judgment on whether someone or something is worth the risk. It is painstaking, unglamorous work—and it is being fundamentally transformed by systems that can process thousands of data points before a human can finish reading a single form.

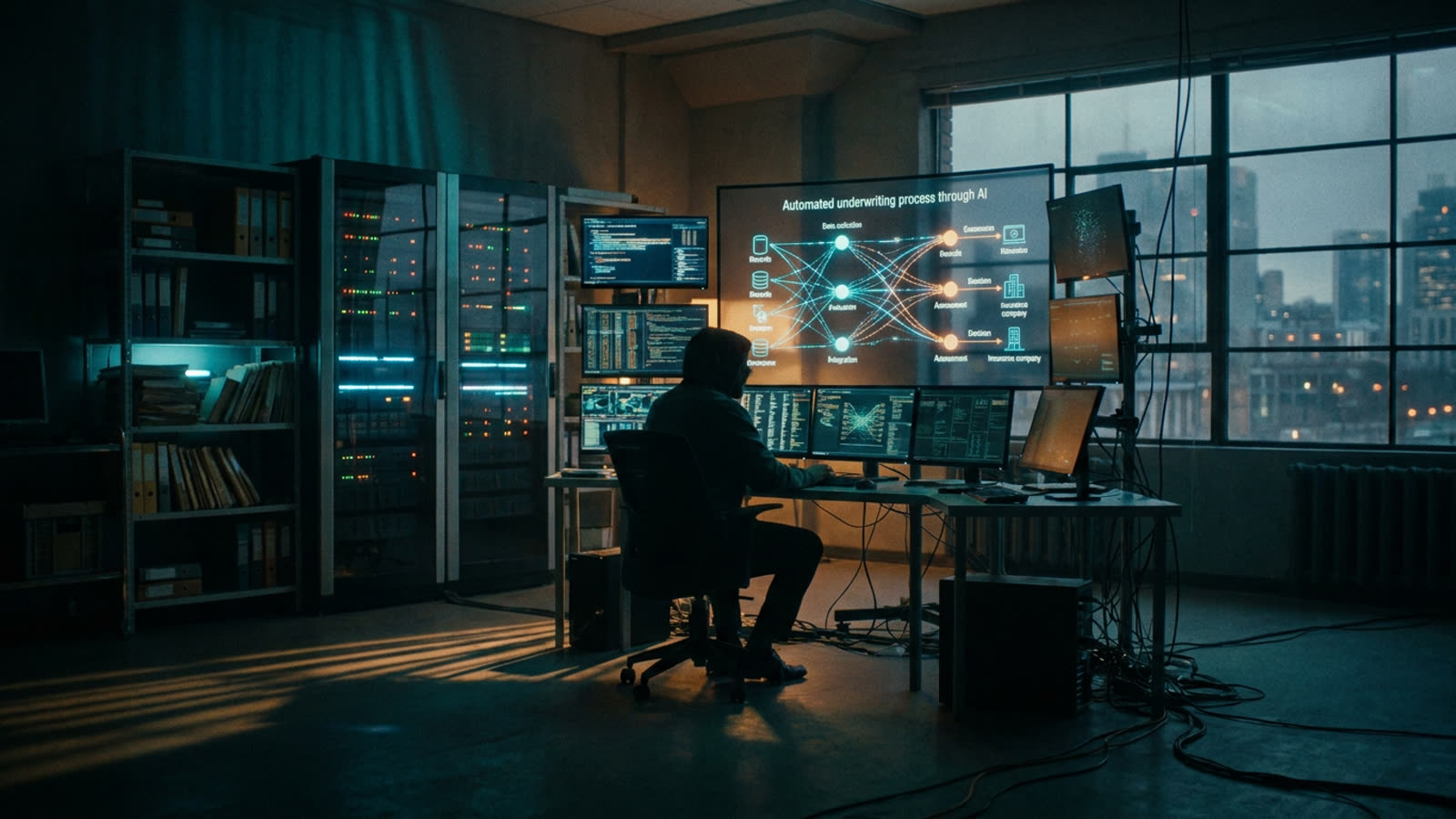

The shift began gradually, with simple automation handling routine tasks. But the current generation of AI tools does something qualitatively different: they identify patterns in risk that human underwriters never saw, cross-referencing variables across datasets that no person could hold in their head simultaneously. A commercial property application that once required a week of analysis can now receive a preliminary risk assessment in minutes.

The new division of labor

What remains for the humans is increasingly supervisory and relational. Senior underwriters at major insurers now spend substantial portions of their time reviewing AI-generated recommendations rather than building assessments from scratch. They become editors rather than authors, catching edge cases the models mishandle and maintaining client relationships that still require human judgment and trust.

This is not the dystopian replacement narrative that dominates AI discourse. Most insurers report that their underwriting headcounts have remained relatively stable even as AI adoption has accelerated. The work has changed more than it has disappeared. Entry-level positions increasingly require comfort with data interpretation and model outputs rather than mastery of traditional manual processes.

Where the machines struggle

The limitations are instructive. AI excels at standardized, high-volume decisions—personal auto insurance, term life policies, routine commercial coverage. It struggles with genuinely novel risks: emerging industries, unprecedented climate patterns, coverage for technologies that did not exist when training data was collected. Underwriting a cryptocurrency exchange or a carbon capture facility still requires human creativity and judgment.

There is also the black-box problem. When an AI system declines coverage or prices a policy aggressively, explaining why to a client or regulator can be genuinely difficult. The models often cannot articulate their reasoning in terms humans find satisfying. This creates friction in an industry where relationships and trust have historically mattered enormously.

The regulatory question

Insurance regulators are watching with a mixture of interest and concern. The efficiency gains are real and potentially beneficial to consumers. But so are the risks: algorithmic bias could systematically disadvantage certain demographics, and the opacity of AI decision-making sits uneasily with disclosure requirements. Several jurisdictions are developing frameworks for algorithmic accountability in insurance, though comprehensive regulation remains nascent.

Our take

The insurance industry's AI transformation offers a useful corrective to both utopian and apocalyptic narratives about automation. The technology is neither replacing human underwriters wholesale nor leaving the profession unchanged. It is doing something more interesting: redefining what the job actually is. The underwriters who thrive in this environment will be those who learn to collaborate with systems that are simultaneously more powerful and more limited than they initially appear. That is a more nuanced story than the headlines suggest, and probably a more accurate preview of how AI will reshape knowledge work broadly.